FAB Market Insights

Stay informed with our art news and market insights.

Following its biggest recession in 10 years, the global art market bounced back to above pre-pandemic levels in 2021, with aggregate sales of art and antiques by dealers and auctioneers reaching $65.1 billion, up 29% from 2020. Yet that recovery was uneven, notes cultural economist Clare McAndrew in the sixth edition of the Art Basel and UBS Global Art Market report.

The auction sector saw the strongest year-on-year advance, with public auction sales of fine and decorative arts and antiques reaching an estimated $26.3 billion, up 47% on 2020. Not surprisingly, there was high demand in both online and offline sales, as well as strong interest in the livestreamed sales format. As for category, the top-selling lots of 2021 were for the most established artists in the Modern and Post-War and Contemporary sectors, among them Pablo Picasso, Jean-Michel Basquiat, Mark Rothko and Cy Twombly.

With just enough high-quality supply and ample demand, the top-tier auction houses reported an influx of new buyers, notably millennials and buyers from Asia who made up one third of all bids by value worldwide and almost half of the bid-on or bought lots over $5 million.

Private sales by auction houses flourished too, increasing by 32% to an estimated $4.1 billion. With owners and collectors mainly stuck at home, private sales teams — who know where many of the top artworks are situated — were able to ramp up their activity. The dealer market also grew and was up by 18%, with aggregate sales hitting an estimated $34.7 billion.

Although the Fine Art Market report does not look at how the war in Ukraine and sanctions on Russian buyers will impact the art market this coming year, Art Basel’s global director Marc Spiegler acknowledges its humanitarian impact in the foreword: ‘As I write this, a human tragedy is unfolding in Ukraine, one which has shocked and enraged us not only as individuals but also as members of a global art community whose values – humanity, pacifism, freedom of expression, cultural understanding, and dialogue – stand in stark contrast with such an unprovoked act of aggression.’

Also absent from the report is any mention of the increasing role of art advisors who continue to provide the inside track to collectors during these changing times. Many advisors, including the team at Fine Art Brokers, have continued to travel to source, view and sell art on behalf of their clients.

Below, we outline five key takeaways from the 2022 Global Art Basel and UBS Fine Art Market Report.

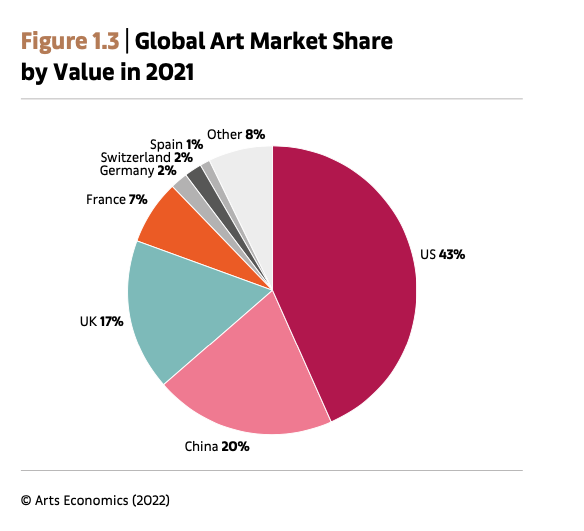

The US market retained its leading position

The US market enjoyed a global market share of 43% in 2021, with art sales topping $28 billion, just below its historic peak of almost $30 billion in 2018.

‘The value of imports of art and antiques into the US rose by 60% year-on-year in 2021, and although they were still below 2019 levels (at $8.3 billion in 2021 versus $11.8 billion in 2019),’ writes McAndrew in the report, ‘the role of the New York market as the headquarters for the international trade in higher-priced works of art was very evident.’ (It’s worth noting that all of the top 10 most valuable lots in 2021 were sold through New York.)

Greater China secured the second-largest market share with 20% of worldwide sales by value at 13.4 billion, while the UK slipped back into third place with a share of just 17% and sales of $11.3 billion. Indeed, it’s been a challenging two years for the UK art market in the wake of the pandemic as well as its formal exit from the EU in January 2021.

‘The impact of Brexit will likely continue to diminish London’s importance in the global fine art market,’ says Ray Waterhouse, co-founder of Fine Art Brokers. ‘France probably benefited from London’s weakened position as it had a particularly good year, with total sales up 50% year-on-year to $4.7 billion, their highest level in 10 years.’

Online sales are still growing

Despite the return of live events, the online market continued to expand in 2021, growing by 7% to reach an estimated $13.3 billion. McAndrew finds that online sales accounted for 20% of sales in the art market, more than double the level of 2019.

As confidence to buy sight-unseen and online grows, digital activity is set to remain an important revenue driver across all sectors this coming year. Some dealers are planning online-only selling exhibitions, while others are investing in digital strategies, including social media, OVRs, direct personal emails and online shops. Livestreamed and online sales will continue at all the top-tier auction houses.

‘It is estimated that e-commerce growth will continue to moderate but stay positive, and that sales could reach $7.4 trillion by 2025 and make up 24% of all retail sales,’ writes McAndrew in the report.

NFTs are going nowhere

The market for digital art also enjoyed an uplift, with the sales of art-related NFTs expanding more than one hundredfold in 2021 to reach $2.6 billion. External sales on NFT platforms on the Ethereum, Flow, and Ronin blockchains grew from $4.6 billion in 2019 to $11.1 billion in 2021.

Such growth was driven by short-term trading, according to McAndrew. ‘NFTs are bought and resold within around one month (versus the average resale period on the art market of 25 to 30 years).’

Christie’s NFT sales totalled $150 million in 2021, buoyed by the landmark $69.3 million sale of Beeple’s Everydays: The First 5000 Days (2021), while Sotheby’s reported NFT sales of $80 million. According to McAndrew, 74% of HNW collectors purchased art-based NFTs in 2021, with the median expenditure across all NFTs reported as $24,000.

Interestingly, over half of the HNW collectors surveyed and 61% of millennial collectors were planning to buy digital art in 2022. Despite this uptick in interest in the category, only 6% of dealers sold NFTs in 2021. A further 19% had not sold NFTs but were interested in doing so in the next one to two years.

But speculation, money laundering, IP theft and high profitability remain areas for concern, with ‘wash trading’ (artificially increasing the value of an item by being on both sides of the transaction) being a notable worry. The environmental impact of mining NFTs is another.

Dealers

‘After a decline of 20% in 2020, aggregate sales in the dealer sector reached an estimated $34.7 billion in 2021, increasing by 18% year-on-year, but still below the level of 2019,’ writes McAndrew. ‘Across all dealers, 55% were more profitable than in 2020, 21% were about the same, and 24% were less profitable.’

Driven by HNW collectors looking for highly priced works, the larger dealers with sales between $5 million and $10 million enjoyed the most growth. Smaller dealers with turnover of less than $250,000 experienced the smallest gains and reported dissatisfaction with the ‘lack of progress toward a more egalitarian model’. It seems the general outlook is optimistic, however, with 62% of dealers anticipating an improvement in sales this year.

The future of fairs

As the art fair calendar resumed in 2021, art fair sales accounted for 29% of gallery sales (including OVRs), up 7% in share year-on-year. And things are looking up: 65% of dealers surveyed predicted their art fair sales would increase over the next 12 months, 11% were unsure, and only 9 % expected a decline.

Although the number of in-person art fairs came in at 240 in 2021, more than one-third down from the 387 recorded in 2019, most galleries surveyed plan to return to the pre-pandemic schedules of fairs and exhibitions this coming year. They will, however, look to update their fair strategies, whether by taking smaller booths, or focusing on more saleable artists to cover costs.